An Ho-4 Insurance Policy Typically Covers Which of the Following

Learn more about sewers and sewer backup insurance. A homeowners policy for example is a package policy typically providing coverage for the perils of fire lightning extended coverages and personal liability.

Types Of Homeowners Insurance Insurance Com Homeowners Insurance Renters Insurance Homeowner

An HO-4 policy may also cover personal liability medical payments and LOU as well.

. Damage to a third-party property for which the insured is legally liable. Sewer backups are not covered under a typical homeowners insurance policy nor are they covered by flood insurance. To get a good grasp at how they differ lets start with all the HO3 policy coverage details.

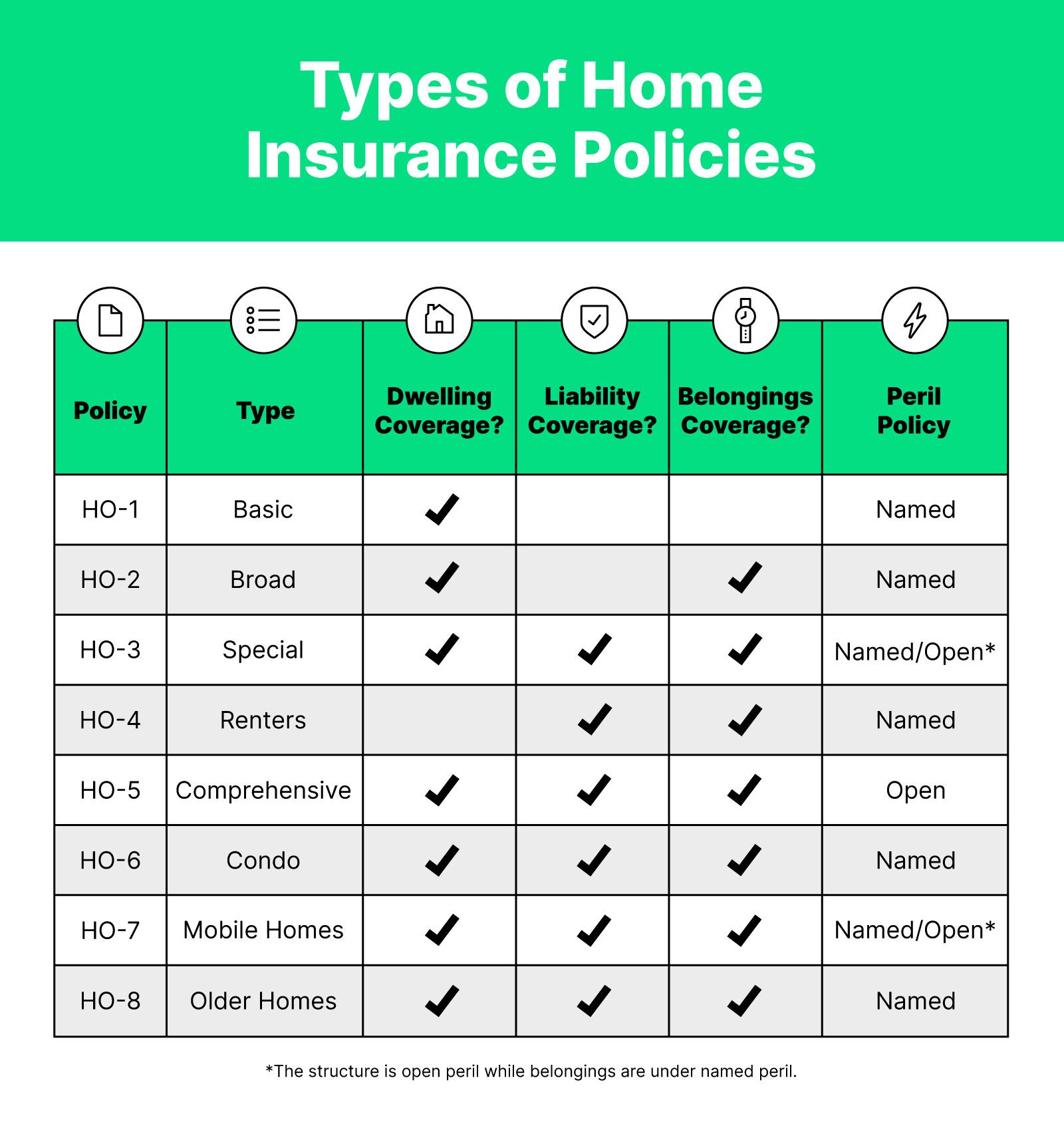

A standard renters insurance policy is also known as an HO-4. Riot or civil commotion. Covers house and contents against 16 perils which are named in the policy.

Covers the structure for all perils except those specifically excluded by the policy. Form HO-2 Check your policy for a complete listing of any perils that may be excluded. Special form homeowners policy.

HO-2 is sometimes called the broad form. Extended coverage include coverage for the perils of windstorm hail explosion riot civil commotion aircraft vehicles smoke vandalism malicious mischief theft and breakage of glass. Condo insurance protects your condominium unit and your personal belongings and covers medical expenses and legal costs if a guest sustains an injury in your unit.

Dwelling coverage is not included in an HO-4 simply because the rental structure would be covered by the landlords insurance. Covers contents for 16. Homeowners insurance covers the cost of repairs or a full rebuild of your home through your policys dwelling coverage if its damaged or destroyed by a fire storm or any other peril.

This policy insures your household contents or personal possessions provides for additional living expenses in the event of a covered loss that makes your home apartment or condominium uninhabitable. Usually the homes are more than 40 years old and do not qualify for an HO-3 policy. An HO-4 does not cover damage to the rental unit.

Like the HO-1 the HO-8 only covers the 11 common perils. HO-8 policies are more affordable because of that smaller payout. It offers no coverage for personal belongings the insured partys liability other parties medical expenses or coverage for accommodations if the home becomes uninhabitable.

HO-4 and HO-6 policies cover personal property against the following named perils. Additional coverages in the liability section of a homeowners policy cover all of the following EXCEPT. This is a more comprehensive version of the HO-3 form.

Both the HO-4 and the HO-6 forms are named peril forms which means the property is insured for damage resulting from certain perils. HO-6 policies are designed as insurance for condo owners and co-op tenants. Texas Type of Coverage Policy Form ISO Policy Form HO-A HO 1 Named perils for both building and contents.

Expenses the insured incurs rendering first aid for bodily injury to third parties. This type of policy form helps protect a renters personal belongings against 16 perils says the III. Contents are covered against perils named in the policy.

An HO-1 homeowners policy is the most barebones option typically sold by insurance companies. This is because it covers the same 10 perils or events as HO1 plus a few extra. Types of insurance for condos and co-ops.

An HO-1 policy only covers the dwelling on a named peril basis a peril is. Knowing the difference between HO3 and HO5 helps you shop for the ideal level of coverage. Subject to the policy limits that apply we will pay only that part of the total of all loss payable under Section I that exceeds the deductible amount shown in the Declarations.

The HO-4 Renters Insurance. The renters landlord would need a separate landlord insurance policy to help protect the structure of the rental property. HO-6 policies cover condominiums co-ops and townhouses.

HO2 is simply one of those forms. For example the following companies cover sudden and accidental discharge or overflow of water or steam but there is no coverage if there is. Most homeowners insurance policies are written on standardized forms.

Most are designed for homes but HO4 is renters insurance HO6 is for condos and HO7 is for mobile homes. The amount of your dwelling coverage typically 10 to 20 percent or for a specific period. It offers HO-3 coverage but also includes.

In total an HO-2 policy covers these 16 perils. These forms make it easier for states to regulate insurance. Unless otherwise noted in this policy the following deductible provision applies.

HO-6 policies work in conjunction with your communitys master policy. It pays to rebuild or repair your house or other structures on your property. Most HO-4 policies also provide liability insurance in case someone is injured in your apartment and provide money for living expenses should you need to stay elsewhere temporarily while the rental property is being repaired or renovated.

This type of coverage must be purchased either as a separate product or as an endorsement to a homeowners policy usually at a nominal cost. The HO-4 policy is a specially designated to meet the needs of a tenant in a rented dwelling by duplicating the coverage of an HO-2 policy without insuring the dwelling itself 15 a tenant is renting a dwelling unit in a condominium. Damage to the property of others.

This is the most comprehensive home insurance coverage you can get.

What Is An Ho 4 Insurance Policy Coverage Com

8 Types Of Homeowners Insurance You Need To Know Hippo

/types-of-insurance-policies-you-need-1289675-Final-6f1548b2756741f6944757e8990c7258.png)

Insurable Interest Definition

Comments

Post a Comment